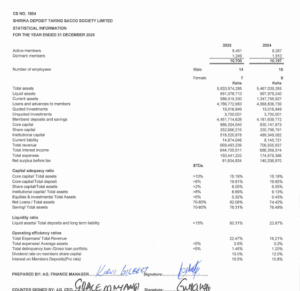

Shirika Deposit Taking Sacco Society Limited has announced its audited financial results for the year ended December 31, 2025, highlighting a period of robust expansion in its asset base and membership despite a tightening of net surpluses. According to the latest statistical information, the Sacco’s total assets climbed significantly to reach Kshs 5.83 billion, up from Kshs 5.46 billion in the previous year.

This growth in assets was largely driven by a sharp increase in credit activity, with loans and advances to members rising by 17.6 percent to hit Kshs 4.78 billion. The Society’s resource mobilization also remained strong, as members’ deposits and savings grew by 6.5 percent to close the year at Kshs 4.45 billion.

On the membership front, the Society crossed a significant milestone by growing its total base to 10,700 members. This 4.9 percent increase was bolstered by a 14 percent surge in active members, who now number 9,451, while the number of dormant members saw a welcome decline of over 34 percent during the period.

While operational scale increased, the Sacco navigated a challenging revenue environment. Total revenue for the year stood at Kshs 669.4 million, representing a 5.2 percent decrease from the Kshs 706.5 million recorded in 2024. Although management successfully reduced total expenses by 13.8 percent to Kshs 150.4 million, the net surplus before tax experienced a 34.7 percent dip, settling at Kshs 91.6 million compared to the previous year’s Kshs 140.3 million.

In light of these results, the Sacco adjusted its returns to members, proposing a dividend rate of 10.0 percent on share capital and an interest rate of 10.5 percent on member deposits. These figures represent slight adjustments from the 12.0 percent and 10.8 percent rates offered in 2024. Despite these shifts, a notable highlight of the report was the dramatic strengthening of the Sacco’s liquidity position, which surged from 23.87 percent in 2024 to an impressive 80.31 percent in 2025, signaling a very robust cash position.

The Society remained fully compliant with all statutory requirements throughout the year. It maintained healthy capital adequacy ratios, with core capital to total assets standing at 15.19 percent and core capital to total deposits at 19.91 percent, both well above regulatory minimums. Additionally, the Sacco successfully managed its credit risk, keeping the total delinquency rate at a low 1.45 percent of the gross portfolio.

The financial statements were prepared by Acting Finance Manager Kirui Gilbert and countersigned by Acting CEO Grace M. Mwangi. The 2025 results underscore a year of strategic consolidation for Shirika Sacco, characterized by increased member participation and a fortified balance sheet.

Sacco Expenses Rise Amid Operational Expansion

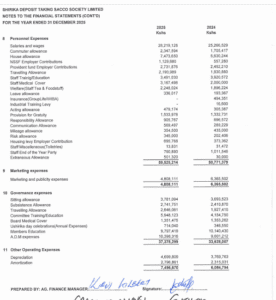

Shrika Sacco’s latest audited financial statements reveal a notable rise in total administrative and financial expenses, reflecting increased operational activity and investments in service delivery. The Sacco spent heavily on key cost centres such as staff-related expenses, office operations, technology systems, and member services during the year under review.

Staff costs and governance-related expenditures formed a significant portion of the administrative outlay, underscoring the Sacco’s focus on strengthening institutional capacity. Expenditure on rent, utilities, and office maintenance also featured prominently, indicating continued branch operations and infrastructure support.

Technology and systems development costs, including software and data processing charges, rose as the Sacco enhanced digital platforms and internal controls. Meanwhile, professional fees, legal charges, and audit costs pointed to a sustained emphasis on regulatory compliance and governance oversight.

The Sacco also recorded increased spending on member engagement activities, training, and cooperative development initiatives, demonstrating a strategic push to improve service delivery and member value.

On the financial expenses front, provisions for loan losses and bank charges contributed to the overall cost structure, reflecting prudent risk management amid a dynamic lending environment.

Overall, the expense profile suggests that Shrika Sacco is investing in growth, operational efficiency, and regulatory compliance. While the higher expenditure may exert short-term pressure on margins, it positions the Sacco to strengthen service capacity, support loan portfolio expansion, and deliver sustainable long-term value to members.